Spell: The Magic Money of the Internet

There is a good chance that you leave this post wondering “Zak, what the hell are you doing in your free time?”. That would be fair. But hopefully this is still a fun and informative post. Also, to be clear, this is not financial advice: We are going to talk about borrowing from a site called abracadabra.money. Anyway, onward.

There are many ways to borrow money, but normally it’s from a bank, against the securities in your brokerage account (or maybe your parents - 👋 mom!). Now there’s another option: abracadabra.money, which is similar in concept to borrowing against the securities in your brokerage account, only instead of stocks, you use cryptocurrency tokens. Are the two comparable? Let’s see:

Based on the pictures, one looks a little more professional, talks about the borrow rate and has a picture of a debit card; and, on the right, we have images reminiscent of Super Mario, discussion of “magic internet money” and a “spell book”.

Right, now that we’re all on the same page now, let’s dive into a few more details.[1]

Borrowing Against Stock

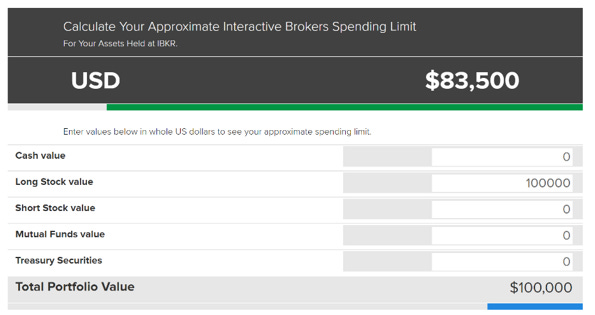

A cheap and potentially effective way to get access to capital is to borrow against your portfolio. If we head over to interactive’s site we can see that for $100k in long stock value, we can borrow up to 83.5%.

To borrow this amount, we would have to pay interest on it, but since capital is so cheap, it might be a better option than having to sell the appreciating asset. The rate for borrowing currently stands at around 1.6%. So, if we were to borrow on 50% of $100k in collateral, in one year’s time we would owe $800 in interest. If we think over the next year we can change our $100k into $101k, it is worth borrowing against these assets rather than selling them because we can always sell the $1k we earned to pay off the debt and keep the delta. We can then use this money to fund purchases, invest more or do whatever it is we want to do with the cash.

It’s great because we don’t have to sell the assets or realize any gains and pay taxes on the gains. The risk is liquidation, but stocks only go up, so we don’t have to worry about that. And if the stocks go up at a faster rate than the borrow rate, borrowing against these assets makes a lot of sense. In recent years, we’ve seen a boom in this kind of borrowing (image to the left). Buy stocks, borrow against them; rinse and repeat.

Beautiful DeFi

A little background might be helpful before we get started on our journey of borrowing against crypto assets in general, and SPELL in particular. [Just to be clear, you may end up with more questions than when we started, but that’s crypto and sometimes it just doesn’t make sense.]

In crypto, there is something called “staking”. Staking just means locking up your assets for a period to earn rewards / interest for providing a service, such as providing liquidity. This interest typically comes from the protocol that is generating revenue for providing a service (e.g., liquidity, lending, etc.). For abracadabra.money, one way it generates revenue is by lending out it’s stablecoin. Like any lender, it collects interest on these loans. If we stake our SPELL, the governance token (we can think share certificate here) of the protocol, we are distributed a percentage of the revenue that abracadabra.money is earning, proportional to the total amount staked. For example, If I stake 10 SPELL in a pool of 100 staked SPELL that generates $100 in revenue, I get $10. We can kind of think of this like earning interest from a deposit account at a bank.

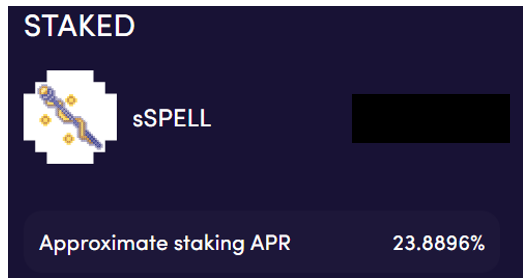

At the time of writing this, the APY is ~23.9% (Disclosure: I currently stake my spell – whatever, leave me alone – this is fun!). Now, we don’t earn dollars for staking, we are paid in the native currency of the protocol. If we stake SPELL, we now hold sSPELL and are paid in SPELL for performing this task. And just like that, we are compounding returns. Outside of earning yield, staking our SPELL allows us to take part in another endeavor: borrowing.

I can take my staked Spell, called sSPELL, and use it as collateral to get magic internet money. We can think of the sSPELL as our stocks / collateral and the magic internet money as USD that we get in return for putting up our cryptocurrency as collateral. The natural thing that comes to mind is all this sounds a lot riskier than borrowing against stocks. Let’s walk through what is happening here: When we stake our sSPELL as collateral, we pick the amount we want to borrow against which sets: 1) our liquidation price – the price drop when our spell is liquidated and sold and 2) the amount of Magic Internet Money (MIM) that we’re allowed to take out. MIM is the stablecoin the protocol issues. For all intents and purposes, it is meant to be equivalent to $1. Thus far, it has done a fairly good job of staying close to $1.

Will this always hold true? Only time will tell, and therefore we want to borrow from the protocol now and take advantage of this opportunity.

Borrowing on abracadabra.money

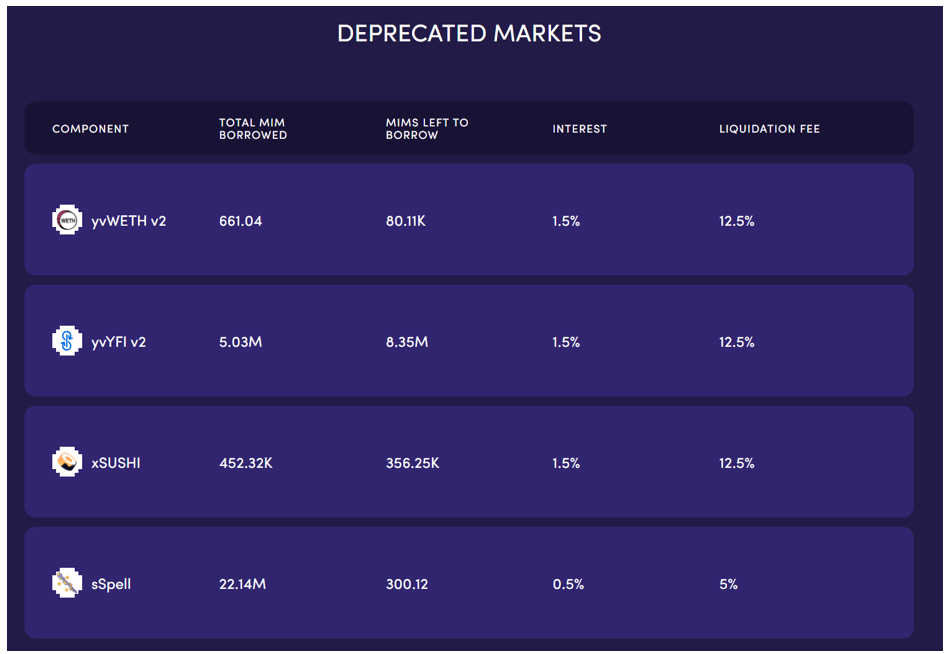

The borrowing pool for sSPELL to MIM allows us to borrow up to 85% of the sSPELL we hold. If we hold $10,000 in sSPELL you can borrow up to $8,500 and only pay 50bps a year on this loan. This is the equivalent process to Interactive Brokers, allowing us to borrow $83k on a $100k portfolio, but at a cheaper rate. All the details on this lending are in the screenshot to the below.

It costs 50bps to borrow and then 50bps a year in debt is accrued. Assuming there is no liquidation, this just means that if we want to get our collateral back – the staked SPELL – we must pay 50bps annually on the amount borrowed. If we borrow $8,500 and come back in a year in which we were not liquidated, we would owe $43 to get our collateral back.

There are a couple of reasons why we might want to borrow against this protocol immediately:

The interest rate is insanely low

who knows if this project survives the next 3 months, and

if the protocol is successful and we aren’t liquidated, we can always pay off our debt and reclaim our SPELL. The riskiest part, to me, is buying SPELL in the first place. If we’re already there, might as well participating in borrowing.

Below is the screen for borrowing money. We aren’t going to borrow the max amount because we are afraid of getting liquidated and losing our collateral. 50% seems right.

We only borrow 50%. At the time of writing this, one staked spell was trading around 2.2 cents and you get liquidated if this price drops to 1.28 cents or falls about 42%. We now have $5k to go and do as we wish. The first thing one might do is go and switch MIM to USDC, a stablecoin fully backed by cash and cash-equivalents. We would do this because most of us (or maybe just myself) feel more comfortable with a stablecoin that is backed by U.S. short term treasury bills and cash than an algorithmic one called Magic Internet Money.

Now that we have USDC, we have an ultra cheap loan to go and do as we wish. We got this amount from putting up collateral on an asset that is volatile and risky. If the price drops 40+ percent, it might be heading to zero because that may mean the rug was pulled, or it might just be from the volatility. Now, the main risk is we get liquidated on a quick crash down, lose our assets, and in a week the token is trading well above this amount. But we still had $5k to go spend on things while this all occurred.

To me, it just seems like a no-brainer to borrow against this asset – and honestly, kind of feels like free money, but maybe that’s just crypto, idk. If we’re long crypto, we can use the stablecoin to go buy more crypto and get leverage; we could even go buy more SPELL, stake this SPELL and get even more leveraged on SPELL. And again, if you get liquidated, you still hold the new asset, unless of course you bought more SPELL. If you don’t get liquidated and SPELL appreciates, you eventually just go pay off your debt and redeem the SPELL. And in order for this all to make sense, we just had to outearn a 50bps loan, which is a pretty low hurdle.

Sadness

As I was writing this, the lending market described above was removed. We can no longer borrow against our sSPELL 😭😭😭 at the liquidation price and rate described above. I will choose to not read too much into this.

Conclusion

Despite just how absurd all this sounds, abracadabra.money is an interesting idea in the crypto space and I’d encourage everyone to read about the project: https://docs.abracadabra.money/.

Appendix

Rejoice! One day later and it looks like they added back this pool with a higher liquidation fee, perhaps suggesting it was a little riskier than how they had priced the initial pool.

[1] I should note: This is not a deep dive into how any of this works but should be a good primer on the overall mechanics and ideas behind using collateral to borrow.

As expected, great stuff Zak!